Connect with us for all your queries

The concept of “income” is the cornerstone of any taxation system, and under the Indian fiscal framework, it forms the very foundation upon which tax liability is determined. The Income-tax Act, 2025, enacted to consolidate and modernise the law relating to income tax, continues to place significant emphasis on defining the term “income” in an expansive and inclusive manner.

Unlike ordinary commercial parlance, where income is generally understood as periodic monetary receipts, the statutory definition under tax law is far more comprehensive. It encompasses not only earnings arising from traditional sources such as salary, business, and investments but also extends to benefits, perquisites, capital gains, digital assets, and even certain receipts without a direct profit motive.

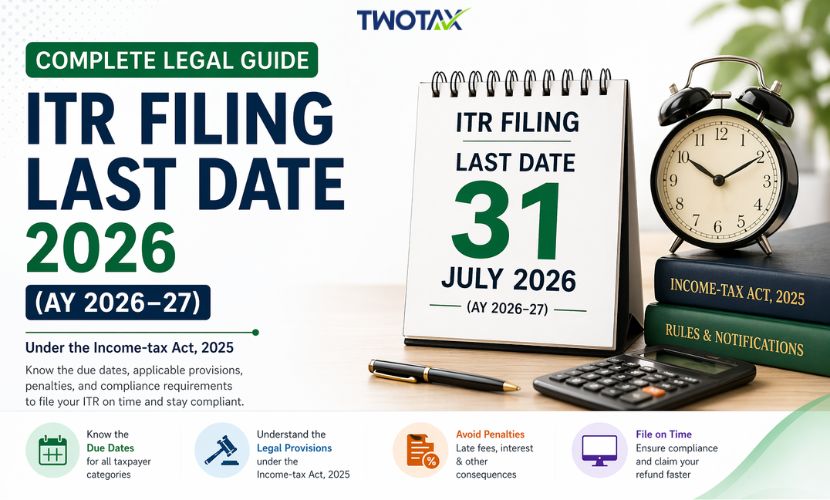

The Act, which comes into force from 1st April 2026, reflects a paradigm shift in taxation by recognising emerging economic realities, including the rise of digital assets and complex financial instruments.

This article undertakes a detailed and structured examination of the definition of income under the Income-tax Act, 2025, analysing its scope, components, legal implications, and practical significance from a professional perspective.

In common understanding, income refers to:

However, under tax law, the meaning of income is:

Thus, the statutory definition overrides ordinary meanings.

The Income-tax Act, 2025 adopts an inclusive definition under Section 2(49), which means:

This ensures:

Section 2(49) provides that income includes various categories such as:

This inclusive framework ensures that virtually every economic gain is brought within the tax net unless specifically exempted.

This is the most fundamental component of income.

It includes:

Key Observations:

Dividend represents:

It includes:

Significance:

Dividend taxation ensures that profits distributed to shareholders are brought within the tax base.

Voluntary contributions are treated as income when received by:

Key Insight:

Even though termed “donations,” such receipts are treated as income to ensure transparency and regulatory oversight.

This includes:

Examples:

Professional Insight:

Tax law recognises economic benefit rather than mere monetary receipt.

Allowances are classified into:

While some are exempt, many are taxable depending on:

Income includes benefits received by:

Even indirect benefits:

Capital gains arise from:

Includes:

Even though capital receipts are generally non-taxable, capital gains are specifically included as income.

Includes:

Income derived from:

is taxable under this category.

Includes:

Such income is:

Employer-collected contributions such as:

are treated as income if:

Any proceeds from such policies are:

Includes:

Exception:

If adjusted against asset cost, it may not be taxable separately.

Tax law includes:

Includes:

A significant inclusion under the new Act.

Covers:

Importance:

Reflects India’s move towards:

As per Section 5:

This establishes:

Taxability is based on:

Includes:

Even if:

It may still be taxed.

Ensures:

.png)

However:

Although the new Act modernises provisions, certain established principles remain relevant:

❌ Only salary is income

✔ Income includes multiple categories

❌ Gifts are exempt

✔ Taxable beyond limits

❌ Digital assets are unregulated

✔ Now explicitly covered

Understanding income helps in:

The 2025 Act:

The definition of income under the Income-tax Act, 2025 reflects a comprehensive, inclusive, and forward-looking approach. By covering traditional as well as modern forms of economic gains, the Act ensures that taxation remains relevant, equitable, and robust.

From a professional standpoint, the key takeaway is:

Any receipt that enhances a taxpayer’s financial capacity, unless specifically exempt, is likely to be treated as income.

This necessitates:

Tax Partner is India’s most reliable online business service platform, dedicated to helping you in starting, growing, & flourishing your business with our wide array of expert services at a very affordable cost.