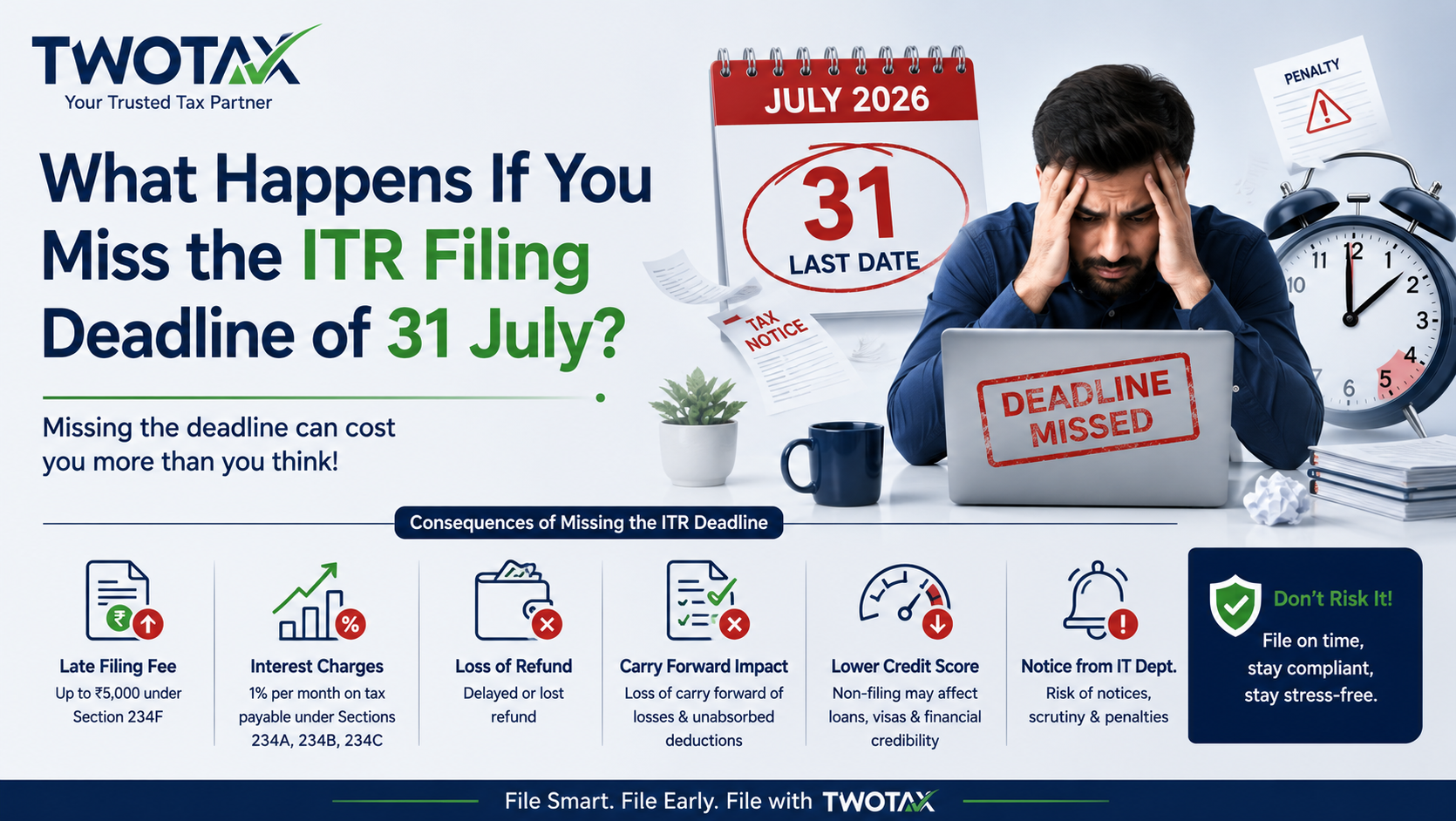

What Happens If You Miss the ITR Filing Deadline of 31 July?

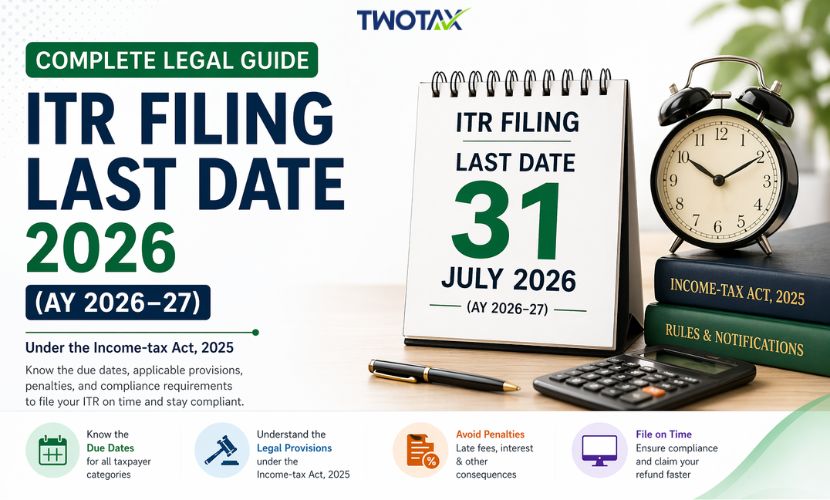

The last date to file your Income Tax Return (ITR) is 31 July 2026 for most individual taxpayers. Learn why timely ITR filing matters, the benefits of filing early, and the consequences of missing the due date.

By CA (Dr.) Arpit Yadav July 15, 2026

Missing the Income Tax Return (ITR) deadline isn’t only about forgetting, it s kinda like a domino effect. It can pull you into extra costs, delayed refunds, trouble with certain tax benefits and honestly, more paperwork that nobody wants. Yes, in many situations you can still file a belated return, but doing it after the due date is almost never a “win”.

Here are a few major outcomes if you miss the 31 July deadline, and what they usually turn into.

1. Late Filing Fee

If you don’t file your ITR by the notified due date, you may need to pay a late fee, as per the Income-tax Act, but only if the relevant conditions and limits apply in your case.

And this isn’t some “instead of” thing. It comes along with whatever tax you already owe, so filing later doesn’t magically erase it.

Example:

Let’s say your tax due is ₹15,000 and you miss the deadline. Besides the tax amount, you might also have to pay the late filing fee plus interest, and overall your outflow goes up.

2. Interest on Unpaid Tax

If any self-assessment tax is still pending after the due date, interest can keep stacking up until the unpaid part is finally cleared.

Even if it looks small at first, the total interest amount can become more noticeable later on.

3. Delay in Receiving Your Refund

For many salaried individuals, TDS is deducted during the year, so the refund is basically “your money back”. But you can only claim that back properly by filing the Income Tax Return.

So if you delay the ITR, the refund also tends to get pushed back.

Instead of getting the refund in a few weeks, you may end up waiting much longer, just because the return went in late.

4. Trouble With Carrying Forward Losses

If you had eligible business losses or certain capital losses in the financial year, then timely filing may be important to carry them forward, so you can set them off in future years, subject to the Income-tax Act rules.

Missing the deadline can mean you lose chances that could have helped reduce taxes later.

5. More Chances of Errors

When you file in a rush, small mistakes become more likely, like:

-

wrong bank account details

-

incorrect PAN or Aadhaar entries

-

deductions getting missed

-

choosing the wrong ITR form

-

forgetting an income stream

-

mismatch in TDS details

These errors may lead to defective filing, notices, slower refunds, or even the need for revisions.

6. Last-Minute Technical Problems

Every year, the Income Tax e-Filing Portal sees a big spike in traffic near the due date.

If you try to file on the last day, you might run into:

-

slow portal performance

-

login issues

-

OTP delays

-

payment gateway failures

-

interrupted uploads

Filing a bit earlier is a simple way to avoid these avoidable tech hurdles.

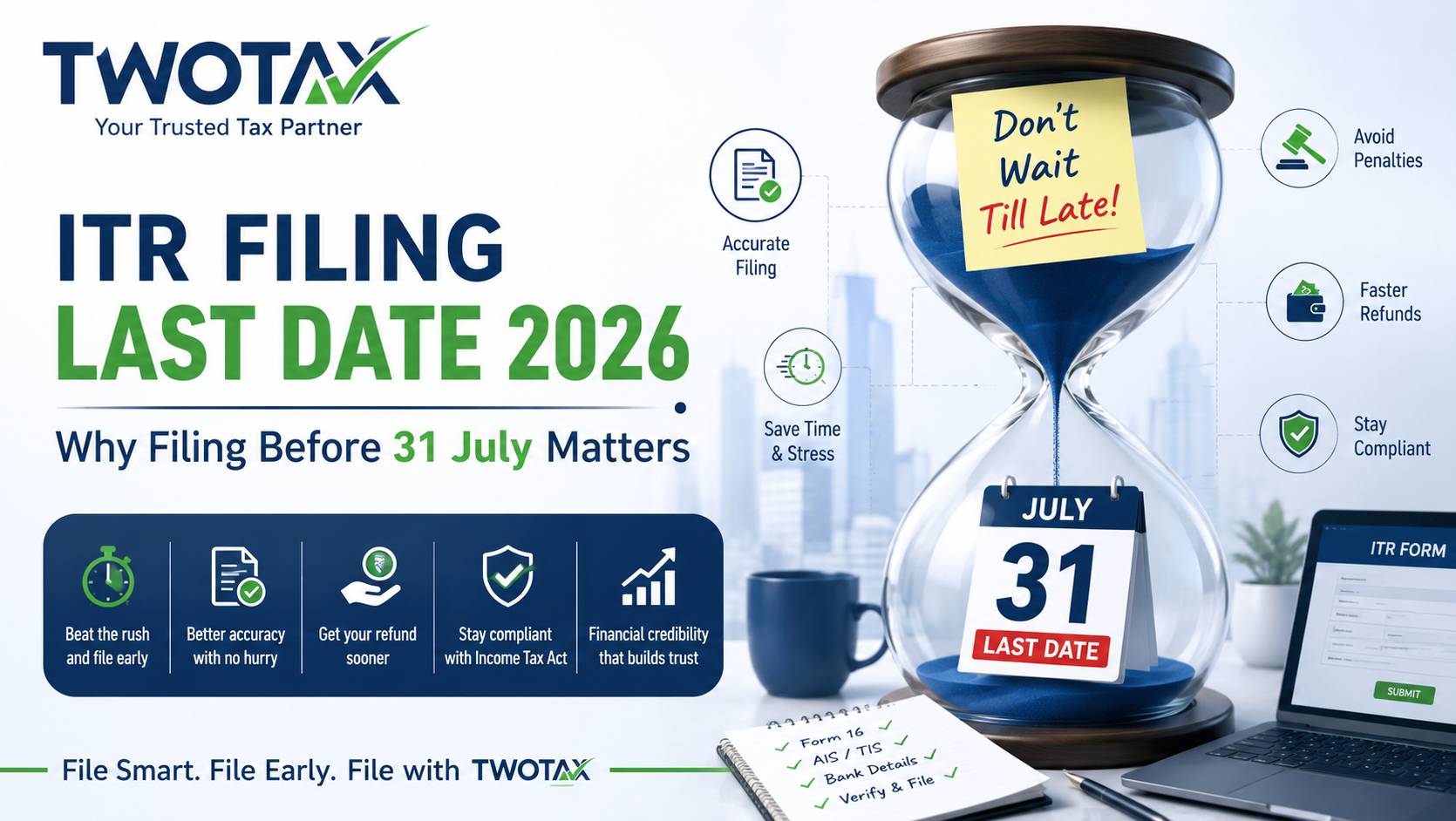

Why Filing Your ITR Early Is Usually the Better Move

Many taxpayers think filing in April and filing on 31 July is basically same, as long as the submission happens before the deadline.

But in real life, early filing gives a few practical advantages.

Faster Processing

-

Returns submitted earlier are often processed sooner, especially when the details match the information available with the Income Tax Department.

-

-

That can mean quicker updates on your return status, and where relevant, faster refund timelines too.

Better Accuracy

-

When you aren’t rushing against the clock, you can double-check properly:

* salary details

* interest income

* dividend income

* capital gains

* rental income

* foreign income, if applicable

* deductions under different sections

* tax credits shown in Form 26AS and AIS

A properly reviewed return tends to reduce the chances of trouble later.

Extra Time to Fix Discrepancies

Sometimes you only notice issues after you start compiling everything, like:

-

TDS not being correctly reflected

-

employer information being off

-

interest income missing from the records

-

bank details needing correction

If you file early, there is usually enough time to correct these points before the due date.

Documents Required Before Filing Your Income Tax Return

Keeping your documents ready before you start can cut down the time you spend uploading and re-checking, and it also improves accuracy.

Below is a basic checklist of commonly needed documents.

|.png)

Once you have these handy, the filing process usually feels smoother, and it becomes easier to avoid missing items.

Common Errors to Avoid While Filing ITR

Even seasoned taxpayers can end up making something off. Usually the same few things happen again and again, like this:

Picking the Incorrect ITR Form

People in different taxpayer categories need to use different ITR forms. If you choose the wrong one, the return can get treated as defective, and it becomes a hassle later

Skipping AIS and Form 26AS

A lot of taxpayers just depend on Form 16.

But then additional income like, savings account interest, fixed deposit interest, dividends, capital gains, and other reported transactions might show up in the Annual Information Statement (AIS). You should really review it before you file, not after

Wrong Bank Details

Refunds fail quite often because an account number is typed incorrectly, or the IFSC code is wrong, even by one character.

So double check the bank details carefully before submitting

Forgetting Other Sources of Income

Income from the following areas has to be included too, where it applies:

-

Freelancing

-

Consultancy

-

Rent

-

Interest

-

Dividends

-

Cryptocurrency (if reportable)

-

Foreign income

-

Capital gains

If you miss some pieces, it can trigger notices or lead to a revised return being required

Not Verifying the Return

Filing the ITR is not the end of it.

After submission, the return usually needs to be verified within the required time limit, using methods like Aadhaar OTP, net banking, or other available options.

If you leave it unverified, it might not be considered as validly filed.

Pro Tips for a More Smooth ITR Filing

Use these practical pointers so the whole thing stays easier and error free:

-

Do not wait until the last week.

-

Download and check your AIS before filing.

-

Match the TDS entries with Form 26AS.

-

Keep supporting documents together in one place folder.

-

Verify bank account details.

-

Recheck deduction claims.

-

Choose the correct ITR form.

-

Review the return before the final submission step.

-

Do verification right after filing.

-

Save the copy of the acknowledgement and computation for later use.

Why Filing Through a Chartered Accountant Can Help

The Income Tax Department does have an online filing system, but many people have income coming from multiple places—investments, capital gains, foreign assets, or even business activities so reporting needs to be handled carefully.

Having professional help can:

-

Spot deductions you may not know about.

-

Lower the odds of mistakes.

-

Ensure income is reported correctly.

-

Handle notices if they come up.

-

Support maximizing genuine tax benefits.

-

Save time and reduce compliance stress

For people with more complicated finances, professional guidance can also add that extra level of assurance that the return was prepared accurately.