Connect with us for all your queries

The introduction of the Income-tax Act, 2025 marks one of the most significant overhauls in India’s direct tax framework in decades. While much of the discussion has focused on simplification and restructuring, one area that deserves special attention is residential status.

At first glance, the rules may appear familiar. However, a deeper look reveals that the new law brings refined interpretations, tighter conditions, and subtle but powerful shifts that can directly affect how much tax you pay.

If you are an NRI, a professional working abroad, or someone with global income streams, these changes are not just technical they are financially critical.

Under both the earlier Income-tax Act, 1961 and the new Income-tax Act, 2025, residential status continues to be the starting point of taxation.

Before calculating income, deductions, or tax rates, the law first asks a fundamental question:

This classification determines whether:

The 2025 Act retains this core principle and continues to define a “resident” and “non-resident” based on prescribed conditions . However, what has changed is how strictly these conditions are interpreted and applied.

One of the most important aspects of the new law is that it does not completely reinvent residential status. Instead, it builds on the existing framework.

The familiar conditions continue to apply:

This continuity ensures that taxpayers are not forced to relearn the entire system. However, relying on this similarity alone can be misleading, because the real shift lies in the details.

The Income-tax Act, 1961 allowed a certain level of interpretational flexibility. Over time, courts and taxpayers developed practices around how residential status could be determined.

The Income-tax Act, 2025 changes this approach.

It moves towards:

This means that while the structure looks the same, the margin for interpretation has significantly reduced.

One of the most impactful changes relates to the exception available to Indian citizens leaving India.

Under the earlier law, the benefit of the extended stay condition (where the 60-day rule was replaced by 182 days) applied to individuals leaving India “for the purpose of employment.”

This phrase was interpreted broadly. Even if a person was travelling abroad in search of employment, they could potentially claim this benefit.

The 2025 Act tightens this provision.

Now, the condition applies only when an individual leaves India for employment outside India.

This change may seem minor in wording, but its implications are significant.

It effectively means:

As a result, many taxpayers who earlier qualified as Non-Residents may now be classified as Residents, exposing their global income to Indian taxation.

Another key shift in the 2025 Act is the emphasis on substance over intent.

Earlier, taxpayers could rely on interpretation and supporting explanations. Now, the law expects:

This means that residential status is no longer just about counting days—it is about proving your position with clarity.

The concept of Resident but Not Ordinarily Resident (RNOR) continues under the new Act, but with improved clarity in its application.

RNOR status has always been a transitional category, offering relief to individuals who:

The 2025 Act refines how this classification is determined, making it more structured and less open to interpretation.

Additionally, the concept of deemed residency, which was introduced to prevent tax avoidance by high-income individuals with no clear tax residence, has been better aligned and clarified.

This ensures that:

One of the most noticeable structural changes in the Income-tax Act, 2025 is the replacement of the dual concepts of “Previous Year” and “Assessment Year” with a single term:

While this may seem like a technical update, it has practical importance.

It simplifies:

For residential status, this means:

The new Act is designed to be more readable and structured.

Key improvements include:

However, this simplification comes with a trade-off.

While the law is easier to understand, it leaves less room for creative interpretation.

This is particularly important for residential status, where even a small misinterpretation can lead to:

The changes introduced in the Income-tax Act, 2025 are especially relevant for individuals with cross-border connections.

For NRIs:

For professionals working abroad:

For frequent travelers:

In all these cases, the risk of being unintentionally classified as a resident has increased.

The Income-tax Act, 2025 does not radically alter the concept of residential status. Instead, it strengthens it.

The shift can be summarised as:

This reflects the government’s broader objective:

to simplify the law while tightening compliance.

Residential status remains the backbone of taxation in India.

But under the new law, it is no longer enough to have a general understanding. Taxpayers must:

Even a small oversight can result in a significantly higher tax liability.

The transition from the Income-tax Act, 1961 to the Income-tax Act, 2025 represents an evolution rather than a revolution in residential status rules.

The fundamentals remain unchanged, but the approach has become sharper, clearer, and more stringent.

For taxpayers, this means one thing:

Accuracy in determining residential status is now more important than ever.

If you are unsure whether you qualify as a Resident, RNOR, or Non-Resident under the new law, it is important to get it right the first time.

At The TwoTax, we assist with:

A correct classification today can save you significant tax tomorrow.

1. What is residential status under the Income-tax Act, 2025?

Residential status determines whether an individual is treated as a resident or non-resident in India for tax purposes. It decides whether a person’s global income or only Indian income will be taxable in India. Under the Act, this classification is based primarily on the number of days an individual stays in India during a tax year .

2. Has residential status changed in the Income-tax Act, 2025?

The core rules for determining residential status remain largely the same as under the 1961 Act. However, the 2025 Act introduces clearer drafting, tighter interpretation, and narrows certain exceptions—especially for individuals leaving India for employment—making compliance stricter.

3. What is the biggest change in residential status under the new Act?

One of the most important changes is the narrowing of the exception for Indian citizens leaving India. The benefit now applies only when a person leaves India for actual employment abroad, rather than merely for the purpose of seeking employment. This makes it harder to qualify as a non-resident.

4. How is residential status determined in India?

Residential status is determined based on physical presence in India. An individual is generally treated as a resident if they stay in India for 182 days or more in a tax year, or meet the combination of stay conditions over the current and preceding years.

5. What is RNOR status and why is it important?

RNOR (Resident but Not Ordinarily Resident) is a special category of residential status. It provides partial tax relief, where certain foreign incomes may not be taxable in India. It is particularly beneficial for individuals returning to India after working abroad.

6. What income is taxable for a non-resident in India?

A non-resident is taxed only on income that is:

Foreign income is generally not taxable for non-residents.

7. What income is taxable for a resident in India?

A resident is taxed on their global income. This includes income earned in India as well as income earned outside India, regardless of where it is received.

8. What is the difference between the 1961 Act and the 2025 Act for residential status?

The fundamental rules remain the same, but the 2025 Act focuses on:

This makes compliance easier to understand but harder to manipulate.

9. Does citizenship affect residential status in India?

No, citizenship does not determine residential status. A person can be an Indian citizen but still qualify as a non-resident, depending on their stay in India during the tax year.

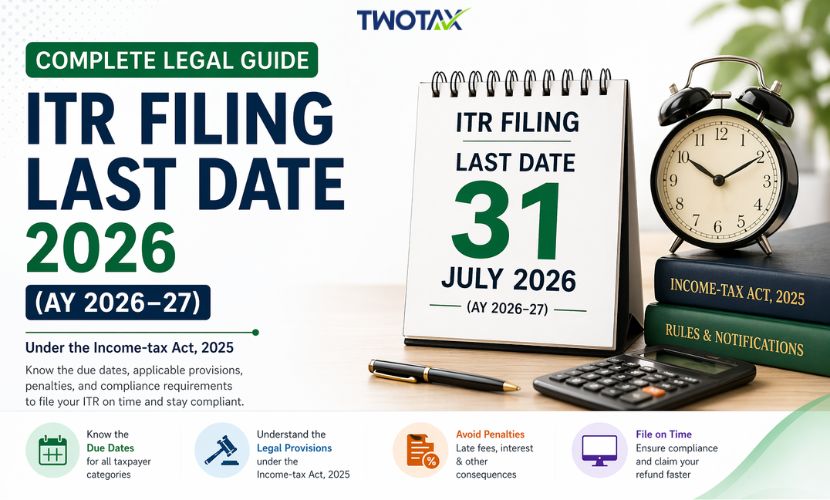

10. What is a tax year under the Income-tax Act, 2025?

The 2025 Act introduces the concept of a “tax year,” replacing the earlier terms “previous year” and “assessment year.” It refers to a 12-month period starting from April 1, simplifying tax calculations and compliance .

11. Can residential status change every year?

Yes, residential status is determined separately for each tax year. It can change depending on the number of days a person spends in India during that year.

12. Why is determining residential status important?

Determining residential status is crucial because it directly affects:

Incorrect classification can lead to penalties or excess tax payment.

Tax Partner is India’s most reliable online business service platform, dedicated to helping you in starting, growing, & flourishing your business with our wide array of expert services at a very affordable cost.