Connect with us for all your queries

1. Understanding the Problem: The Inverted Duty Structure (IDS)

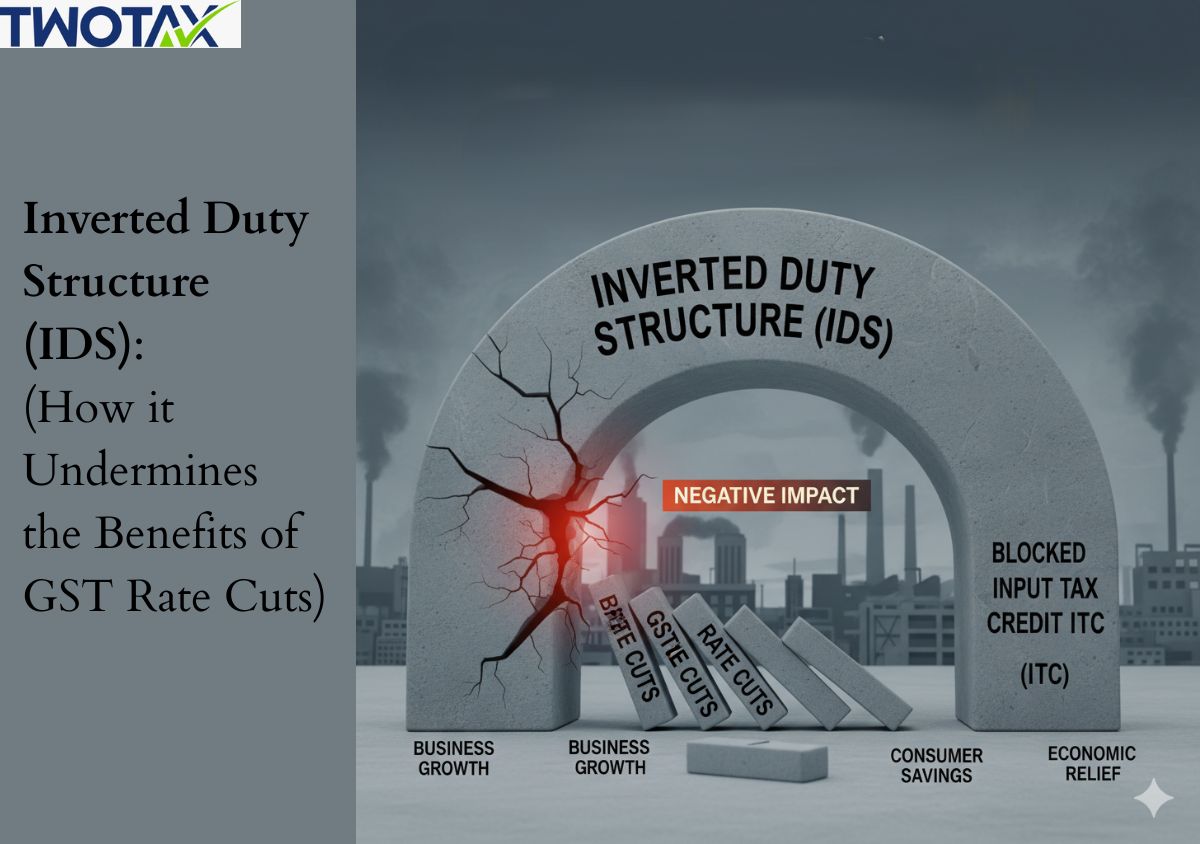

When India introduced the Goods and Services Tax (GST), the goal was simple ,make taxation smoother, fairer, and more efficient by removing the problem of “tax on tax.”

The key to this efficiency is the Input Tax Credit (ITC). Think of ITC as a prepaid balance in your “tax wallet.” Every time a business buys raw materials, machinery, or services, it pays GST on them. Later, when the business sells its final product, it can use that prepaid GST balance to pay the tax on the sale.

If everything works as planned, no one pays more tax than necessary ,the system just passes the tax along the chain until the final consumer pays it.

But here’s the catch: for this system to work, the GST you pay on your purchases (inputs) should roughly match the GST you collect on your sales (outputs). When that balance breaks ,trouble starts.

An Inverted Duty Structure (IDS) happens when the GST rate on your inputs (what you buy) is higher than the GST rate on your outputs (what you sell).

For example:

Now, you’ve paid more GST on your inputs than you can recover on your sales.

Here’s a real example:

A manufacturer of fabric bags pays 12% GST on the non-woven fabric they buy, but the final bags they sell are taxed at just 5%. That 7% difference gets stuck as unusable tax credit.

That “stuck” tax credit becomes money trapped in the system.

Businesses can’t use it, can’t get it back easily, and yet it’s money they’ve already paid. This means less cash for salaries, raw materials, and day-to-day expenses ,a real working capital crisis.

Over time, that blocked credit becomes part of the cost of production. And since no business can sell at a loss, this “extra cost” gets added to the product’s price tag.

So ironically, when GST rates on finished goods are kept low to make them affordable, the price to the consumer doesn’t actually fall ,because manufacturers have to recover their hidden costs from somewhere.

When the GST Council reduces tax rates on items ,say, from 12% to 5% ,it’s usually done to make those goods cheaper for consumers.

But if the inputs for that product are still taxed at 18%, the gap widens. The more the government tries to make the product affordable, the more credit gets stuck in the manufacturer’s account.

So instead of becoming cheaper, the product often stays the same price ,or even becomes slightly costlier over time.

Let’s take an example.

Earlier, a company had inputs at 18% GST and sold outputs at 12%.

The gap was 6%.

Now, if the output rate is reduced to 5%, that gap jumps to 13%. That’s a 13% credit sitting idle ,meaning less working capital and more financial stress.

It’s especially painful for small businesses, which don’t have large reserves to absorb these shocks.

In theory, lower tax rates should mean cheaper goods. In reality, manufacturers can’t pass on those savings because they’re busy covering the cost of stranded tax credits.

Larger corporations can sometimes balance this out by offsetting credits across different product lines, but small and medium businesses ,especially those selling essential goods ,end up losing the most.

That’s why after so many rate cuts, consumers often ask, “Why didn’t the prices drop?”

The GST law does allow refunds for these unused tax credits under Section 54(3).

But there’s a catch ,the formula for refund (under Rule 89(5)) is complex, the paperwork is heavy, and refunds take months to process. Many businesses simply give up or face long waits for their money.

The law allows refunds only for GST paid on goods, not on services or capital goods.

So, if a company spends on rent, logistics, or consultancy ,all taxed at 18% ,they can’t claim that back.

This hits modern, service-heavy industries the hardest ,like pharmaceuticals, IT-based manufacturing, or hospitality ,where services form a large part of total costs.

In 2021, the Supreme Court ruled in Union of India v. VKC Footsteps that these refund restrictions are valid. The Court said that refunds are not a “right” but a policy choice ,meaning only Parliament can change it.

However, the Court did urge the GST Council to reconsider, recognizing the unfairness this causes to businesses.

Sectors like textiles, footwear, and fertilizers have been long-time victims of the inverted duty structure.

In both cases, domestic manufacturers struggled, and exports became less competitive.

In recent years, the GST Council corrected some of these distortions:

These fixes improved competitiveness and boosted exports ,proving that aligning input and output rates works better than simply cutting rates.

GST 2.0 isn’t just another rate revision ,it’s a structural overhaul.

The government aims to:

This approach aims to stop the problem before it starts, instead of patching it later with refunds.

The Supreme Court’s decision made one thing clear ,the law itself needs an amendment.

GST 2.0 is expected to expand the definition of “Net ITC” to include credits on services and capital goods, especially for industries suffering from IDS.

That would be a game-changer for sectors like IT-enabled services, pharmaceuticals, and advanced manufacturing ,where service inputs form a large cost component.

Apart from rate alignment, GST 2.0 plans to automate refund systems to reduce human interference, delays, and disputes.

It also proposes data-driven modeling ,predicting in advance how rate changes might create new IDS situations, and fixing them proactively.

When GST rates are cut without fixing the input-output mismatch, businesses end up with blocked capital and consumers see no price drop.

True reform lies not in rate reduction, but in rate alignment.

GST 2.0 is India’s chance to correct this ,by ensuring:

The path to a fairer GST lies in removing the structural flaws, not just tweaking the numbers. Only when GST 2.0 bridges this gap will India have a truly transparent and growth-friendly tax regime.

Tax Partner is India’s most reliable online business service platform, dedicated to helping you in starting, growing, & flourishing your business with our wide array of expert services at a very affordable cost.