Connect with us for all your queries

The introduction of the Income-tax Act, 2025 marks a major transformation in India’s taxation framework. Designed to replace the Income-tax Act, 1961, the new legislation seeks to simplify tax laws, modernize compliance, and align India’s taxation system with contemporary economic realities.

While structural reforms and simplification are central features of the new law, one of the most important changes lies in the clarification and expansion of key definitions.

Definitions are the foundation of any legal framework, particularly in taxation. The meaning assigned to terms such as “income,” “assessee,” “capital asset,” or “person” determines how tax provisions are interpreted and applied.

In the past, ambiguities in definitions often led to interpretational disputes, litigation, and compliance challenges. The Income-tax Act, 2025 attempts to address these issues by strengthening the definitions framework and presenting key terms with greater clarity.

This article explores the importance of definitions in tax law, the key definitions under the new Act, and how clearer definitions can reduce disputes and improve compliance.

Tax legislation relies heavily on defined terms. Many provisions in tax law operate only after specific terms are interpreted correctly.

For example, determining tax liability may depend on whether a particular receipt qualifies as income, whether a person qualifies as an assessee, or whether an asset falls within the definition of a capital asset.

If these definitions are unclear or open to interpretation, disputes between taxpayers and tax authorities become inevitable.

Historically, several tax disputes in India arose because different parties interpreted definitions differently.

For instance:

Such ambiguities often led to lengthy litigation before tax authorities, tribunals, and courts.

Recognizing this issue, the Income-tax Act, 2025 aims to provide a stronger definitional framework that reduces ambiguity and improves interpretational clarity.

The expanded definitions section in the new law serves several important objectives.

Clear definitions help ensure that tax provisions are interpreted consistently across different situations.

Many tax disputes arise because terms are interpreted differently by taxpayers and tax authorities. Clarifying definitions reduces the scope for such disputes.

When taxpayers clearly understand the meaning of important terms, they can comply with tax provisions more confidently.

Clear definitions ensure that tax policies are implemented as intended by lawmakers.

Overall, strengthening the definitions framework helps create a more predictable and transparent tax system.

The new Act elaborates several key definitions that form the backbone of India’s income-tax framework.

Some of the most important definitions include:

Each of these definitions plays a crucial role in determining how taxation applies to different individuals, entities, and transactions.

The term “assessee” refers to a person who is liable to pay tax or comply with tax provisions under the law.

Under the tax framework, an assessee may include:

The definition also covers situations where a person may be responsible for tax compliance even if the income does not belong directly to them.

For example, a person may be treated as an assessee if they are responsible for deducting tax at source or representing another taxpayer.

A clear definition of assessee ensures that the scope of tax liability and compliance responsibilities is properly identified.

The concept of income lies at the heart of the taxation system. Determining what constitutes income is essential for calculating tax liability.

Income under tax law generally includes various categories such as:

However, the concept of income is broader than merely earnings or profits.

Certain receipts that may not appear to be traditional income can still fall within the scope of taxable income under specific circumstances.

By providing a clearer and more comprehensive definition of income, the new Act aims to ensure that taxable receipts are identified consistently and accurately.

The term capital asset is another critical definition in income-tax law.

Capital assets generally include property held by a taxpayer, such as:

Transactions involving capital assets often give rise to capital gains, which are taxed under specific provisions.

The classification of an asset as a capital asset determines how gains from its transfer will be taxed.

Clarifying the definition of capital asset helps reduce disputes regarding:

This is particularly important in modern financial markets where new types of assets continue to emerge.

Tax liability is imposed on a person, and therefore defining who qualifies as a person under the law is essential.

The definition of person typically includes:

A comprehensive definition ensures that all relevant entities fall within the scope of the tax framework.

It also helps clarify which entities are responsible for filing returns and complying with tax provisions.

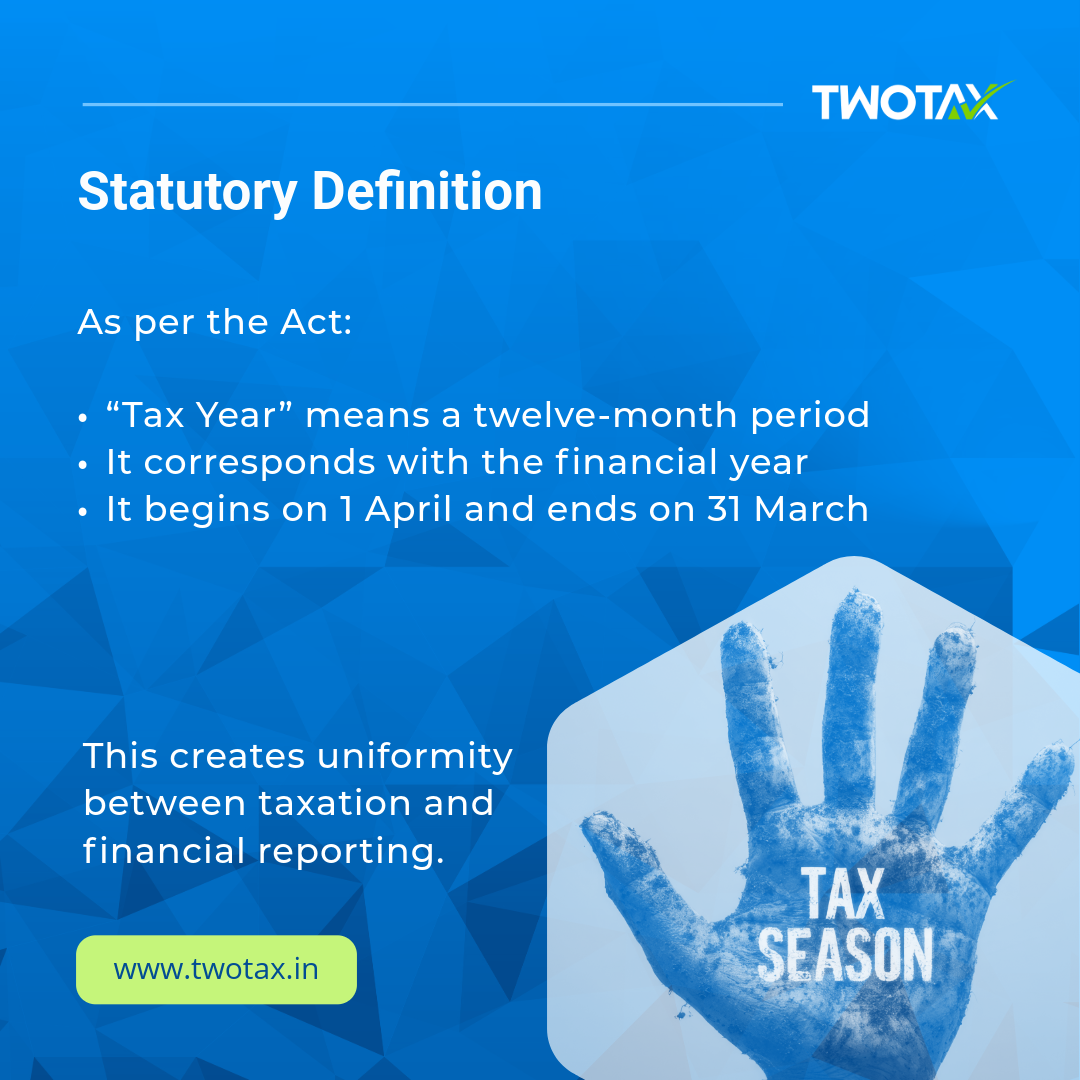

The concept of the previous year plays a fundamental role in determining the period for which income is assessed.

In simple terms, the previous year refers to the financial year in which income is earned.

The income of the previous year is assessed to tax in the assessment year that follows.

For example:

Clarifying the definition of previous year helps ensure consistency in tax computations and reporting obligations.

The modern economy has introduced several new forms of income and financial transactions.

These include:

As new economic models emerge, tax laws must adapt by clearly defining how such income and assets should be treated.

The Income-tax Act, 2025 recognizes the importance of defining concepts in a way that accommodates evolving economic realities.

This helps ensure that the tax system remains relevant in a technology-driven economy.

One of the major challenges in tax administration is litigation arising from interpretational disputes.

Many tax disputes occur because provisions depend on definitions that are open to interpretation.

For example:

By strengthening the definitions framework, the new Act aims to reduce the scope for such disputes.

Clear definitions promote consistent interpretation and help both taxpayers and tax authorities apply the law more effectively.

The enhanced definitions structure under the Income-tax Act, 2025 offers several potential benefits.

Taxpayers can better understand their obligations when key terms are clearly defined.

Clear definitions help taxpayers comply with tax provisions more confidently.

Fewer interpretational ambiguities can lead to fewer tax disputes.

A well-defined framework strengthens the overall integrity of the tax system.

Tax professionals will play a crucial role in helping taxpayers interpret and apply the definitions provided under the new law.

Businesses may also need to review their tax planning strategies to ensure that their transactions are aligned with the definitions specified in the new Act.

Over time, clearer definitions are expected to make tax advisory and compliance processes more efficient.

The Income-tax Act, 2025 received Presidential assent in 2025 and is expected to come into effect from 1 April 2026.

The transition period allows taxpayers, professionals, and businesses to familiarize themselves with the new provisions and definitions before the law becomes operational.

The Income-tax Act, 2025 represents a significant step toward modernizing India’s tax framework. By strengthening the definitions section, the new law lays a strong foundation for clearer interpretation and consistent application of tax provisions.

Definitions such as assessee, income, capital asset, person, and previous year form the building blocks of the taxation system. Clarifying these terms helps reduce ambiguity, improve compliance, and minimize disputes.

As India prepares for the implementation of the new tax framework from April 2026, understanding these foundational definitions will be essential for taxpayers, professionals, and businesses alike.

In the upcoming parts of this series, we will continue exploring the key provisions of the new law to help readers better understand India’s evolving taxation landscape.

Tax Partner is India’s most reliable online business service platform, dedicated to helping you in starting, growing, & flourishing your business with our wide array of expert services at a very affordable cost.